financial fears of the top 5%

turns out it wasn't the end of the world when i dropped down two tax brackets

Lifestyles of the rich and the famous

They’re always complaining, always complaining

If money is such a problem

Well, they got mansions, think we should rob them

“Lifestyles of the Rich & Famous”

Good Charlotte

Two years ago, I lived an extremely cushy life. Not as-seen-in-media-about-NYC life, but a cushy life regardless. I regularly ate out at restaurants with friends and considered “saving money” to be subscribing to Rent the Runway instead of buying new clothes. My definition of “budgeting” was glancing at my bank accounts every month after auto-deposits were diverted towards being responsible (retirement, HSA, student loan repayment, credit cards, rent) and gauging my emotional reaction: phew, we’re okay or crap, gotta spend less next month.

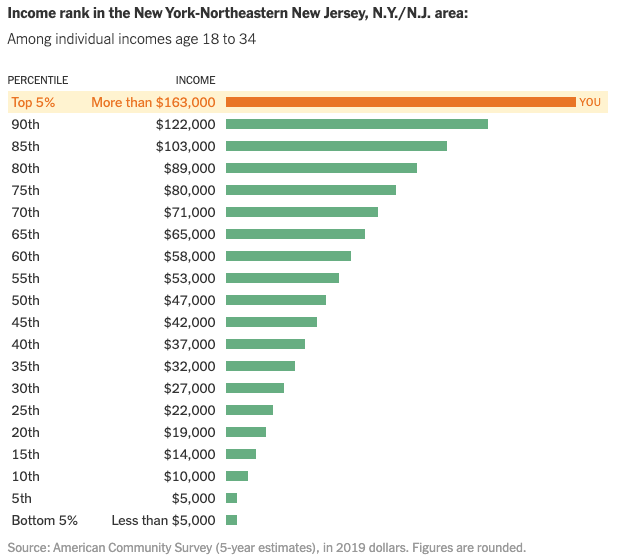

From the outside, you would think that I didn’t worry about money. I was a fifth-year associate at a biglaw firm. I had stayed long enough to reap the rewards of the larger salary increases in between years 3-4 and years 4-5. I even went on a reduced-hours schedule of 80% to accommodate a much lesser-paid teaching position at Yale. Who would do that if they were scared of money? Perhaps being in the top 5% of earners in the New York/New Jersey area meant that I would finally feel like I had enough.

This is by no means a flex. The top 5% percentile for people ages 18-34 is more than $163,000 and the top 5% percentile for people ages 35-64 is more than $239,000—even a brand new first-year associate in biglaw would be in or near the top 5%. The idea of being in the top 5% used to be a marvel; several graduations later, it was the new normal. All of my colleagues were in the top 5%, if not the top 1%. It just was.

Before I knew many rich people, I thought they weren’t scared of money like I was scared of money. I thought there was a discernible level of income when I could breathe a sigh of relief and say to myself, Ah, I’ve made it—I can relax now. The partners seemed to have achieved that nirvana; I asked around the firm for accountant recommendations once and ended up speaking with a partner’s accountant who told me candidly, “Look, I don’t do taxes for your level of assets.” I assumed that the magic number lay somewhere in between my level of assets and the partner’s level of assets.

The magic number, however, didn’t exist. At least not for me. My parents had freaked me out so much about money growing up that I couldn’t emotionally tolerate any form of financial planning except for my rudimentary and unscientific glance-and-feel method of budgeting. Some people told me about FIRE (Financial Independence, Retire Early), where you save an enormous percentage of your income in order to live off of the interest and savings at a much earlier age than traditional retirement, but I couldn’t even calculate what my ideal lifestyle’s expenses in a year would be.

I was so scared, so anxious, so worried about money that I could never look at it. It felt like a phobia—in the same way that claustrophobes spiral when in enclosed spaces and seek escape immediately, I felt the same way when faced with financial decisions. I would copy my officemate’s paperwork when it came to tax withholdings and retirement savings allocations; if I thought about buying something for too long, I would mentally give up, hit Check Out, and hope that I could afford it on the other side. (Thank god I made so much—without that privilege, I would undoubtedly be in mountains of credit card debt.)

I thought that by making a lot of money, I would no longer be scared of money. That was wrong. My fear of money existed regardless of whether I had no money as a high schooler or a lot of money as a biglaw associate. And my fear of money has been with me for a long, long time—I am 32, and I have never filed my own taxes.

Unsurprisingly, leaving biglaw triggered my financial anxiety:

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

Those first months were incredibly uncomfortable. I felt panicked all the time and like I would die. I thought about asking for my job back every single day. The only reason I didn’t was because as much as money scared me, humiliation scared me even more—the thought of having to publicly announce I was abandoning my sabbatical only a few months in was too harrowing. (Strangely enough, in that way the haters living in my head actually helped push me forward.)

Another weird benefit of staying the course in my discomfort: it’s coincidentally the therapeutic prescription for anxiety. By experiencing life without a consistent income, I was unintentionally forcing myself to confront my financial fears and engaging in exposure therapy.

And it worked.

Today, I’m two tax brackets lower than when I made the most. It sounds terrifying—where did all the money go??—but doesn’t actually feel terrifying. I still go out to eat with friends. I still buy the occasional bag or jewelry. And for the first time in my life, I’m actively tracking all my investments, debt, and spending. I can actually look at my money and not want to look away immediately.

That sounds small, but it’s actually a Big Freaking Deal for me. Someone once asked me what my net worth was, and I couldn’t respond—I made an offhand joke about probably negative because of student loans—but the truth then was that I didn’t know, was too scared to know. My truth now?